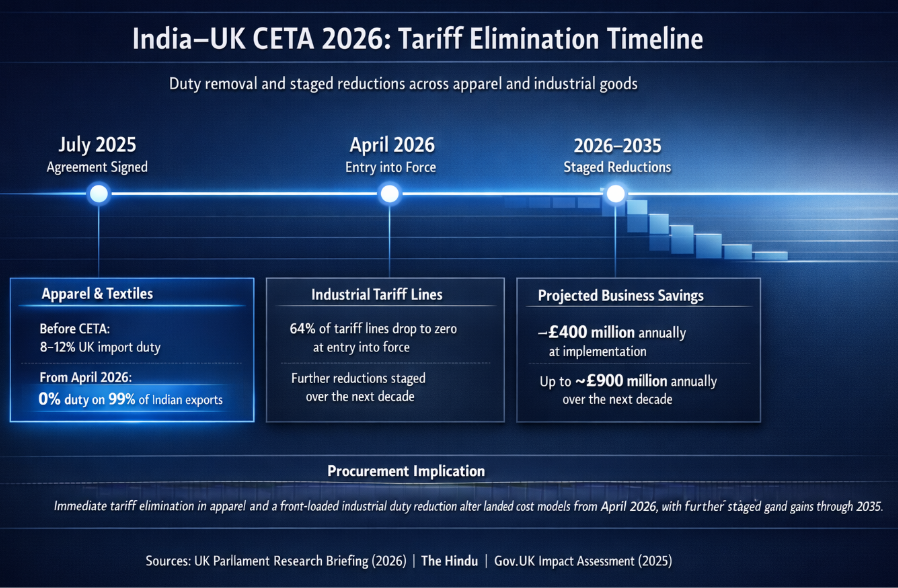

The India-UK Comprehensive Economic and Trade Agreement (CETA), signed in July 2025 and scheduled for implementation in April 2026, alters tariffs and customs mechanics for apparel and industrial sourcing. For UK manufacturers sourcing precision components, the impact is immediate and measurable. Duty removal reduces landed costs on affected tariff lines from day one, without staging or transitional quotas. Where duties previously ranged from 2% to 8%, depending on each’s classification, the elimination directly alters the cost models used in supplier evaluation and contract negotiation.

The treaty provides a new level of parity and speed for everyone involved in sourcing apparel or industrial components. The next few months will be a turning point as these developments will offer a significant opportunity to optimise landed costs and improve delivery timelines. Here is the analytical breakdown of what this means for global buyers.

Capitalising on tariff parity in apparel

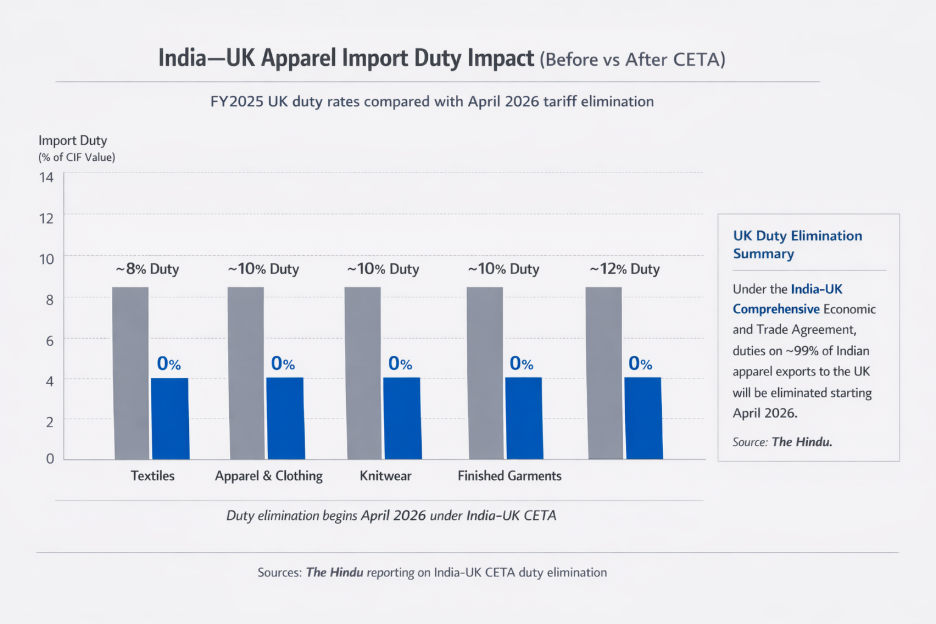

Indian apparel and textile manufacturers have long maintained a reputation for high-quality material and ethical production. However, these goods often faced import duties in the UK, ranging from 8% to 12% that often impacted final pricing. The CETA removes this final barrier to entry. Starting in April 2026, 99% of Indian exports to the UK will enter at 0% duty (The Hindu). This is not just a small change but a total reset that allows India to compete on a level playing field with any other nation.

What this means for apparel buyers

1. Margin optimisation

The removal of duties allows for immediate price parity with competitors in the region. This enables buyers to prioritise India’s vertically integrated fibre-to-fashion capabilities without a cost penalty.

2. Diversification

Buyers can move production to India to de-risk their supply chains without losing their competitive edge on price.

3. True price discovery

Buyers and fashion brands no longer have to weigh India’s superior cotton quality against a 10% duty cost. The competitive price they see is the price they eventually pay.

Industrial goods: the “first-mover” advantage

While textiles get much of the attention, the impact on industrial components is even more significant. On the very first day of the deal, 64% of tariff lines will drop to zero (UK Parliament Research Briefing, 2026). This includes a vast array of machinery, aircraft parts, and electrical components.

For UK-based manufacturers, the cost implications are immediate. Sourcing precision parts from India will become more efficient and affordable overnight. The India-UK agreement removes 64% of tariff lines immediately, compared with staged reductions in other recent trade frameworks.

Official projections suggest that businesses will realise savings of approximately £400 million annually at the start of the program. This figure is expected to reach £900 million over the next decade as further staged reductions occur.

Key industrial sector gains

Engineering goods

Indian engineering exports to the UK are expected to grow. This includes everything from iron and steel products to complex automotive parts.

Technical parity

As duties fall, the incentive for Indian manufacturers to conform to UK technical standards increases. This creates a unified market for technical goods.

The “hidden” value: solving the bureaucracy tax

Experienced buyers know that taxes are only part of the cost. The real challenges are often port delays, paperwork, and social security costs. The CETA addresses these through two major updates.

1. Origin self-certification

Bureaucratic delays at ports often lead to missed production deadlines. The new deal permits exporters to self-certify the origin of goods, replacing the previous requirement for third-party government certificates for every shipment.

Operational impact: This change reduces port processing time by an estimated 48 hours. For industrial buyers, time saving is vital for maintaining just-in-time inventory levels.

2. The double contributions convention (DCC)

The DCC is a critical addition for firms buying complex machinery. Under current rules, Indian technicians working on UK soil for installation or maintenance often face dual social security taxes.

Cost savings: The DCC removes this double taxation. It is projected to save companies over ₹4000 crore annually (Economic Times).

Service efficiency: Lowering the cost of technical movement makes after-sales support and on-site engineering more affordable for UK firms.

3. It quantifies “speed to market”

The deal includes a commitment for customs authorities to release goods within 48 hours (Gov.UK Impact Assessment, 2025). Standard media focuses on the 0% tariff, but for an apparel brand managing a “seasonal” capsule collection, the real value is in the reduction in port dwell times. Self-certification removes the need for a government official to sign off on every batch, which is often the cause of shipping delays.

4. “Bilateral cumulation” highlights

Verified documents show that the CETA allows for bilateral cumulation (EEPC India, 2026). This is a vital technical point for an industrial audience.

Strategic value: If a UK-based manufacturer uses Indian-made components to build a machine, those components are treated as “originating” in the UK.

The benefit: This makes it easier for the final product to meet the 40% to 50% value added threshold required for further trade, allowing UK manufacturers to count Indian inputs towards origin thresholds for third-country exports.

The advantage of legal protection

Legal stability is the most valued asset in the current trade environment. While other trade frameworks face judicial delays or unexpected regulatory changes, the India-UK CETA is a formal treaty-backed instrument. Once the UK Parliament completes the final review process this spring, the rules become a permanent part of the trade architecture.

This provides a secure environment for signing multi-year sourcing contracts. Leaders can plan for the long term with the knowledge that the current tariff rates are protected by international law.

| Category | Previous Rate | Post-April 2026 Reality | Strategic Benefit |

| Apparel | 10% – 12% | 0% | Global price competitiveness |

| Machinery | High/Complex | Immediate 0% / Self-Cert | Reduced lead times and cost |

| Automotive | Over 100% | Phased to 10% (Quota) | Predictable long-term supply |

| Tech Services | Double Taxation | Single Contribution (DCC) | Lower cost of technical support |

The 2026 trade deal establishes India as a primary, high-value hub for global procurement. It is a necessary partner for any firm seeking a balance of quality and cost. With the removal of duties on apparel and the simplification of industrial regulations, the path to a deeper trade partnership is open. The value lies in the elimination of friction and the legal stability provided by this modern treaty.

Leave a Reply